Bridge Report:(7685)BuySell Technologies The Second Quarter of Fiscal Year Ending December 2024

![]()

Chairman Kyohei Iwata |

President & CEO Kosuke Tokushige | BuySell Technologies Co., Ltd (7685) |

|

Company Information

Market | TSE Growth Market |

Industry | Wholesale (trade) |

Chairman and Representative Director | Kyohei Iwata |

President, Representative Director & CEO | Kosuke Tokushige |

HQ address | PALT Building, 28-8, Yotsuya 4-Chome, Shinjuku-ku, Tokyo |

Year-end | End of December |

Homepage |

Stock Information

Share Price | Shares Outstanding (Term-end) | Total Market Cap | ROE (Act.) | Trading unit | |

¥5,360 | 14,310,691 shares | ¥76,705 million | 17.5% | 100 shares | |

DPS (Est.) | Dividend yield (Est.) | EPS (Est.) | PER (Est.) | BPS (Act.) | PBR (Act.) |

¥30.00 | 0.56% | ¥153.34 | 35.0x | ¥589.51 | 9.1x |

* The share price is the closing price as of September 13. ROE and BPS were taken from the brief report on the financial results in FY 12/23. Other figures are from the brief report on the financial results in 2Q of FY 12/24. The number of outstanding shares excludes the number of treasury shares.

Earnings Trend

Fiscal Year | Net Sales | Operating Income | Ordinary Income | Net Income | EPS | DPS |

December 2020 | 14,764 | 968 | 922 | 565 | 41.12 | 7.50 |

December 2021 | 24,789 | 2,315 | 2,295 | 1,314 | 93.26 | 14.00 |

December 2022 | 33,724 | 3,694 | 3,672 | 2,268 | 158.28 | 20.00 |

December 2023 | 42,574 | 2,796 | 2,754 | 1,453 | 100.11 | 25.00 |

December 2024 Est. | 61,850 | 4,680 | 4,140 | 2,240 | 153.34 | 30.00 |

* The estimated values are based on the forecasts made by the Company. On January 1, 2021, a 2-for-1 stock split was conducted. EPS and DPS were adjusted retroactively.

This Bridge Report presents BuySell Technologies’ financial results for the second quarter of the fiscal year ending December 2024 and so on.

Table of Contents

Key Points

1. Corporate Overview

2. The Second Quarter of Fiscal Year Ending December 2024 Earnings Results

3. Fiscal Year Ending December 2024 Earnings Forecasts

4. Conclusions

<Reference: Regarding Corporate Governance>

Key Points

- Cumulative results for 2Q of FY12/24 show a 46.8% year on year increase in sales, reaching 28,720 million yen, and an 84.2% year on year increase in operating income, amounting to 2,420 million yen. With the impact of the inclusion of new subsidiaries in the scope of consolidation, both sales and operating income in the three months of 2Q reached their highest-ever quarterly levels. Compared to the revised budget disclosed in May (sales: 27,263 million yen, operating income: 1,547 million yen), these figures exceeded the projections by 5.3% and 56.4%, respectively. Although this is a period for laying the groundwork for future growth, strong performance is evident.

- In the previous fiscal year, KPIs such as the number of inquiries and visits for the home visit purchase business were sluggish until September due to the incidents of large-scale theft and the extreme heat. However, the recent business environment has been showing signs of improvement. Measures are also being taken to reduce the volatility in the number of visits, particularly addressing the seasonal decline in 3Q.

- The company has announced the acquisition of REXT HOLDINGS Co., Ltd., which owns reuse-related companies and functional companies, including REGATE, which operates the home visit purchase service "Kaitori Fuku-chan," and Nikkodo, which runs an antique purchase business. The profits and losses will be included in the scope of consolidation from 1Q of FY 12/2025. This acquisition will not only strengthen the company’s presence in the home visit purchase sector, but is also expected to expand its business in the field of antiques. Furthermore, synergies are anticipated in areas such as efficient management, data-driven strategies, and the advancement of human resources across various fields.

- Considering the recent performance, the company’s forecast for FY 12/2024 has been revised upwardly once again, following the adjustment in May. Sales are expected to increase 45.3% year on year to 61,850 million yen, operating income 67.4% year on year to 4,680 million yen, and adjusted EBITDA 58.5% year on year to 6,332 million yen. The dividend forecast per share has been raised from 25 yen/share to 30 yen/share. The company maintains its stance, viewing FY 12/2024 as a period of preparation for entering into a high growth phase from FY 12/2025, with the strategic goal of increasing operating income per employee. The company also plans to make upfront investments for FY 12/2025 and beyond. Specifically, the company plans to invest in the opening of flagship stores to strengthen direct-to-consumer sales, the expansion of overseas sales channels, and the strengthening of its own e-commerce.

- With the external environment clearly improving, the company appears to be taking a more assertive stance. While recent performance has been strong, the management is focusing on the future. The capital market should also look beyond short-term results to the company's growth potential. The company’s forward-looking investments indicate an intention to expand beyond the purchase sector. The domestic reuse market is large, and the potential market, including surrounding businesses, is significant for the company. Internationally, Japanese secondhand goods are highly regarded particularly in Asia, and the company expects that its ongoing investments will further expand its total addressable market (TAM).

1. Corporate Overview

BuySell Technologies operates reuse business that leverages the strengths of the "Internet" and "Real world". The Company attracts sellers through a marketing strategy that makes full use of the Internet and mass media, and also provides the home visit purchase service throughout Japan. Its characteristics or strengths include the maximization of synergy with a variety of purchase and sales channels, the robust customer base centered around seniors, and the high-quality management. The Company is aiming for further growth by developing a huge potential reuse market and creating new businesses utilizing its customer base.

[1-1 History]

Mr. Iwata (currently Chairman and Representative Director of BuySell Technologies Co., Ltd.), who was in charge of marketing at a major advertising company, questioned the situation where large and famous companies with abundant advertising expenses are favored to the disadvantage of small and medium-sized companies and start-ups with a small budget. He retired from the major advertising company and established a consulting company for his desire to help companies, including ones with weak capital, develop true marketing. He met BuySell Technologies (formerly Ace Co., Ltd.) while supporting many start-ups and small and medium-sized businesses. The Company had long been providing the home visit purchase service, which is its current core business, but when Mr. Iwata's consulting engagement started in May 2016, its marketing depended almost entirely on flyers. The homepage was not sophisticated, and the business performance was not good.The Company, which undertook a full-fledged reform under Mr. Iwata, began to see the results when it registered a record number of applications in August of the same year, renewing the record in September. In this process, Mr. Iwata felt that while "the home visit purchase service" has a high added value and there are many customers who need it, the way in which the benefits of the service are communicated, the brand is constructed, marketing actions are taken, and others were extremely inadequate. He was convinced that with his marketing know-how, the Company could transform itself into a more attractive company. In October of the same year, Mr. Iwata assumed the role of Chief Sales and Marketing Officer (CSMO). In November, the Company name was changed to BuySell Technologies, and a new TV commercial was put on air and the reform sped up.He assumed the post of president in September 2017. The business expanded steadily thanks to the success of conducting the PDCA cycle of creative activities and the purchase of TV commercials utilizing his expertise. The Company also established a compliance system and was listed on the Tokyo Stock Exchange Mothers in December 2019. In April 2022, the company got listed on the Growth Market of TSE through the stock market restructuring.In April 2024, in order to continue to strategically expand the scale of the group's operations and organization, Mr. Kosuke Tokushige was invited to become President, Representative Director & CEO, and Mr. Iwata was appointed Chairman and Representative Director.

[1-2 Corporate Philosophy and Management Philosophy]

The Company upholds the following missions and values.

Mission:Our Mission | Transcend people, transcend time, become a bridge connecting precious things. |

Value :What We Aim to Be | 1. Hospitality We listen to others and provide them with joy and delight that exceeds their expectations. 2. Professional Maximize your performance by leveraging your professional knowledge and skills. 3. Creative Without being bound by existing concepts, we discover challenges ourselves and create new value. |

The Company believes that things have value that goes beyond their physical existence, and that properly connecting them is its mission and social existence value. In addition, the company is strongly aware of the need to address environmental issues and co-create with all stakeholders, and considers its group mission to be "contributing to the creation of a recycling-oriented society through the revitalization of the secondary distribution market to realize a sustainable society" and "pursuing sustainable growth and maximizing corporate value as a company that co-creates value with various stakeholders including customers, shareholders, employees and society.

Furthermore, the company intends to reflect the value in its human resources evaluation system and link them to the development of next-generation human resources.

[1-3 Market Environment]

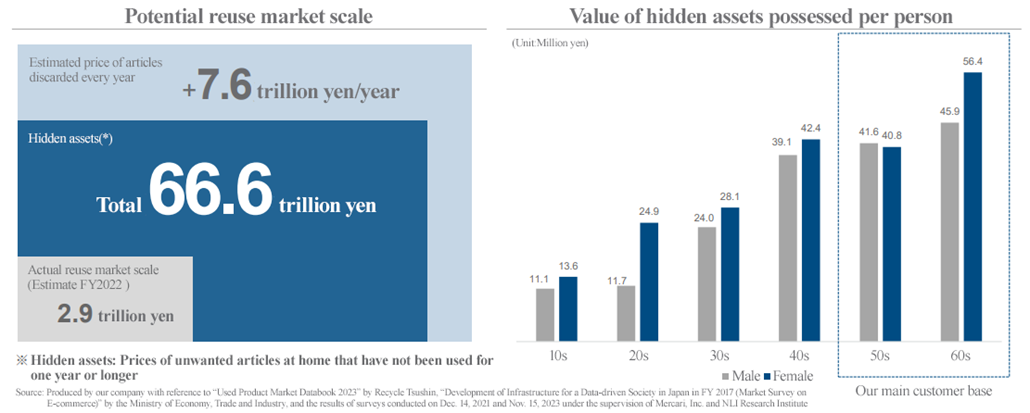

The scale of the reuse market is estimated to be about 2.9 trillion yen in 2022 and is expected to grow to 4 trillion yen by 2030.

However, this is only a figure for the actual reuse market, and the total potential size of the reuse market, including "hidden assets," which are unused items in houses that have not been used for more than one year, is estimated to be over 66 trillion yen. In addition, in Japan, where the population continues to shrink, disused articles are estimated to increase by 7.6 trillion yen each year, and the potential reuse market is expected to continue expanding. In terms of hidden asset holdings per capita in each age group, seniors in their 50s and older hold a significant portion.

The company intends to cultivate the reuse market, which has great potential for growth, by focusing on home visit purchase, which is one of the company's strengths, and by uncovering potential "hidden assets" in the home.

[1-4 Business Description]

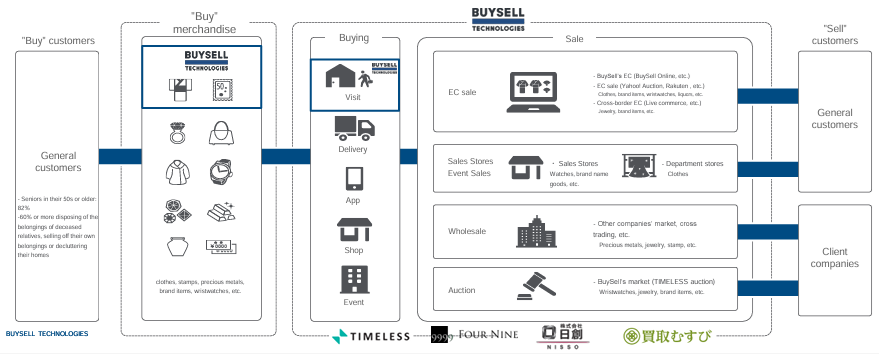

(1) Business Model

The company and its 6 subsidiary, TIMELESS, BuySell Link Inc., FOUR-NINE, Inc., Nisso Co., Ltd., and Musubi Co., Ltd. operate the reuse business by utilizing respective strengths in the Internet and in real transactions. (BuySell Link Inc. is a special subsidiary for the purpose of promoting the employment of people with disabilities.)

It attracts sellers through a marketing strategy that makes full use of the internet and mass media, and also provides a shipping purchase service and a store purchase service as well as the home visit purchase service delivered by its assessors who can travel throughout Japan.

The Company sells purchased products to general customers (toC sales) though EC sales at EC malls such as the Company's own EC site “BuySell Online and BuySell brandchée” and Yahoo! Auctions, and at cross-border EC sites such as eBay, and special event sales at department stores. In addition, it sells to external vendors through the “Timeless Auction", which is held by TIMELESS Corporation, which was acquired as a subsidiary, and wholesale using other companies' markets.

(Source: the reference material of the Company)

The Company has built a system to consistently manage and execute the entire flow from marketing to attracting customers, purchase appraisal, inventory management, and sales on its own. At the same time as expanding its mainstay reuse business, the Company is also focusing on launching and developing new business adjacent to the reuse business and other services utilizing customer data.

(2)Overview of Each Service

The Company's reuse business consists of the following business flo "Attracting sellers" → "Conducting purchase" → "Selling purchased products". The outline and features of each step of "customer attraction", "purchase" and "sales" are described in detail below.

(Source: the reference material of the Company)

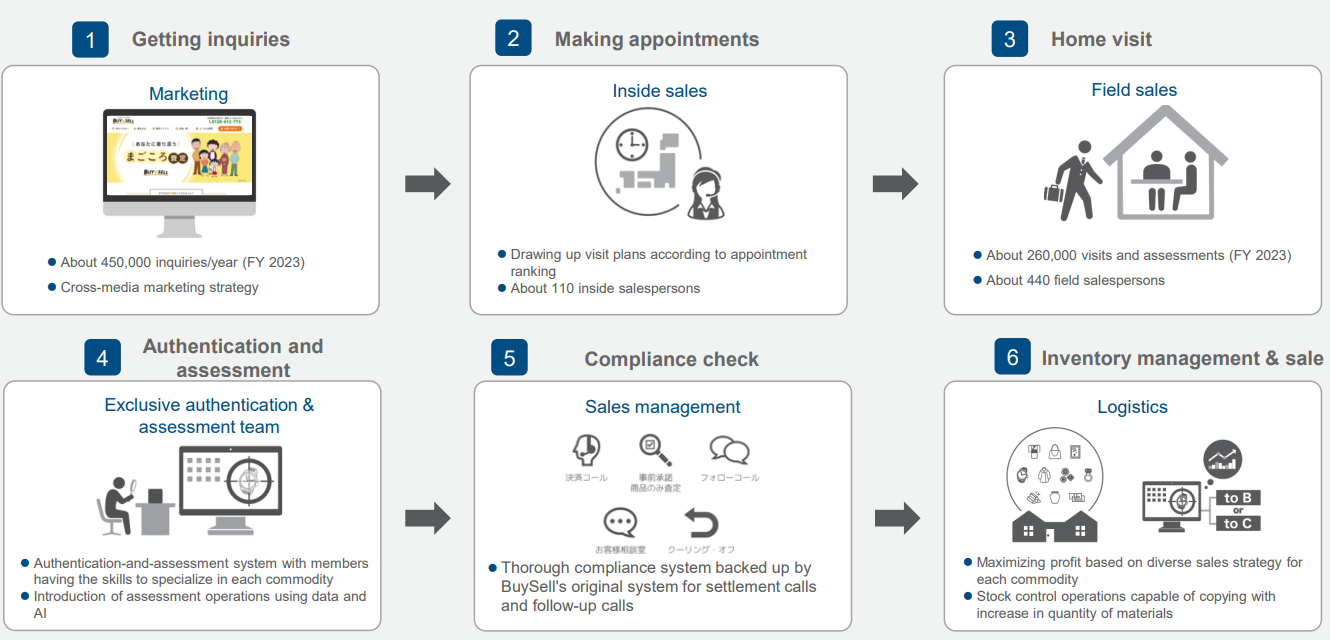

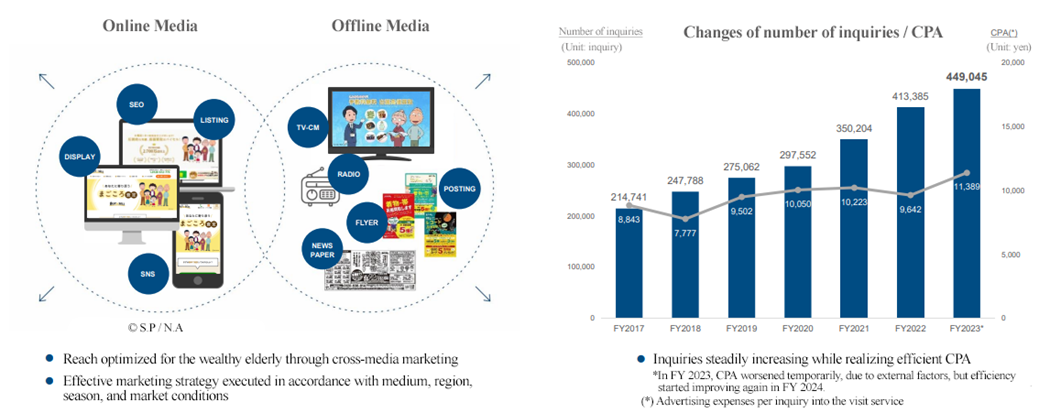

1) Attracting Customers: Developing cross-media marketing aimed at high-net-worth seniors

◎Marketing

Marketing activities for receiving appraisal requests from customers are the starting point of the business strategy and execution, and maximizing the number of customers is the first key to the success of the Company's business.

The marketing skills and know-how possessed by Chairman Iwata, President Tokushige, and the rest of the management team play a major role here.

The Company develops cross-media marketing that leverages "the Internet", such as SEO (Search Engine Optimization), listing ads, and SNS, as well as "the mass media" centered on TV commercials, foldouts, flyers, etc. In addition to advertising operation from a macro perspective based on market conditions and seasonality, the company conducts detailed analysis for each kind of daily media, area, etc., to realize efficient CPA (cost per action) and maximize cost-effectiveness in its marketing activities. Due to such detailed marketing activities, the number of inquiries and customers are increasing year by year.

(Source: the reference material of the Company)

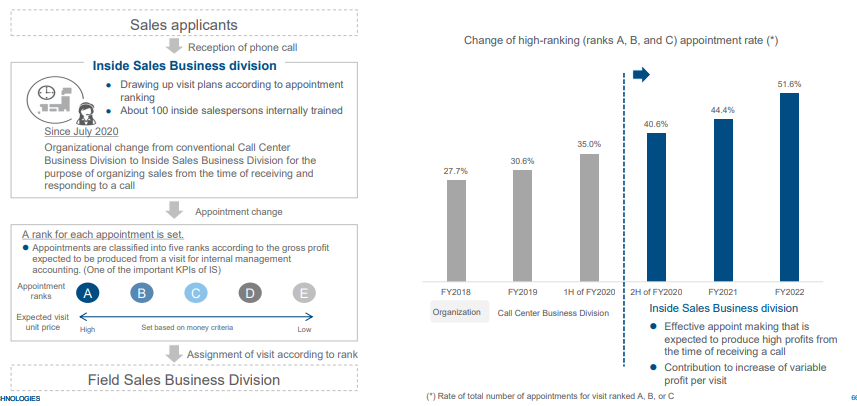

◎Inside Sales: Providing services that meet customer needs and maximizing the efficiency of assessor operations

In response to incoming calls from potential buyers, the company approached through marketing, approximately 100 operators listen directly to customers’ requests and cooperate with assessors to provide services in line with customer needs.

In July 2020, the organization was changed from the previous "Call Center Business Division" to the "Inside Sales Division" for the purpose of organizing sales from the time of answering the first inquiry call.

Moreover, the call center not only performs administrative tasks such as receiving inquiries about products to be sold and arranging the date and time of visits, but also provides the customer with an explanation that will be given when they are visited by an assessor, as well as an overview of the Company's services, information regarding the range of products that can be assessed, and a guidance for preventing uninvited solicitations so that customers can use the Company's services with greater confidence.

In addition, the Inside Sales Division, along with these customer-oriented services, generates highly profitable and effective appointments by classifying them into five ranks based on the expected gross profit per business visit (expected cost per visit) when the call is received.

This organizational change has resulted in a steady increase in the ratio of highly ranked appointments over the years, contributing to an increase in variable profit per at-home visit.

The company receives 449,000 calls (The Fiscal Year Ended December 2023 Results) for asking about purchase per year, and records all of them, to trace the subsequent appointments and home visits. With this, they extract common items and essential points from highly ranked appointments, and educate operators about them. By repeating this cycle, they increase gross profit from home visits.

(Source: the reference material of the Company)

2) Purchase: Developing the "home visit purchase service" meeting a wide range of customer needs

◎The Home visit purchase Service

"The home visit purchase service" which involves going to the homes of customers who made inquiries and conducting an appraisal and a purchase, is the main purchasing method.

In addition, the Company also carries out a "shipping purchase service", in which customers send products to be sold to the Company, and a "store purchase service", in which customers bring products directly to the Company.

The Field Sales Division, which is in charge of "the home visit purchase service," has approximately 439 assessors as of the end of 2023, with based in the Kanto, Kansai, Nagoya, Fukuoka, and other areas, to cover all parts of Japan. "The home visit purchase service" can flexibly respond to purchase requests from customers who have difficulty using store purchases service or shipping purchase service and meet a wider range of customer needs, such as when there is a wide variety of products to be assessed, the quantity of appraisals is large, it is difficult to carry the products due to their weight, as well as when there are inquiries from distant customers and elderly customers. For example, if a customer wants to sell a large number of kimonos which weighs approximately 1 kg per piece, and it is difficult to carry them, "the home visit purchase service" in which the Company's assessor visits a customer's home to conduct an appraisal and a purchase, is highly compatible with such customer needs.

◎Assessor

The number of field sales assessors is also increasing steadily in parallel with the expansion of business scale, based on the company's recruiting capability. Since 2017, the company has been strengthening its recruitment of new graduates.

The company also focuses on the training of assessors to enhance customer satisfaction.

The Sales Enablement Department, a division specializing in education and training, has introduced a systematic education and training system for assessors and implements education and training programs tailored to each assessor in each center, based on the company's unique internal management index.

Considering the shortening of the training period as a KPI, they constantly review their educational programs. Several years ago, the training period was about 6 months, but currently, it is about 5 months.

The Company emphasizes the education of assessors and regularly conducts on-the-job training, including sales skills training and on-site training, to improve sales attitude, appraisal skills, and compliance awareness.

In addition, the Company is working to achieve thorough compliance because the Company must provide customers with safety and security when its employees visit customers’ houses.

The assessors alone cannot make a decision on the contract, and the compliance department calls the customer at the time of the contract and issues a decision call to confirm the contents of the sales contract (confirmation of the product, the price and the customer's satisfaction with the price), after which the contract is finalized.

Furthermore, the compliance department calls the customer again (follow-up call) after the assessor has left to receive the customer's candid opinions about the home visit purchase service, specifically about the assessor's attitude, compliance and customer satisfaction and so on.

The results of follow-up call, including customers’ voices, complaints and compliments are managed for each assessor, and the assessors are thoroughly informed of these to further improve their performance.

The company is also working to ensure that it complies with the cooling-off policy in accordance with laws and regulations.

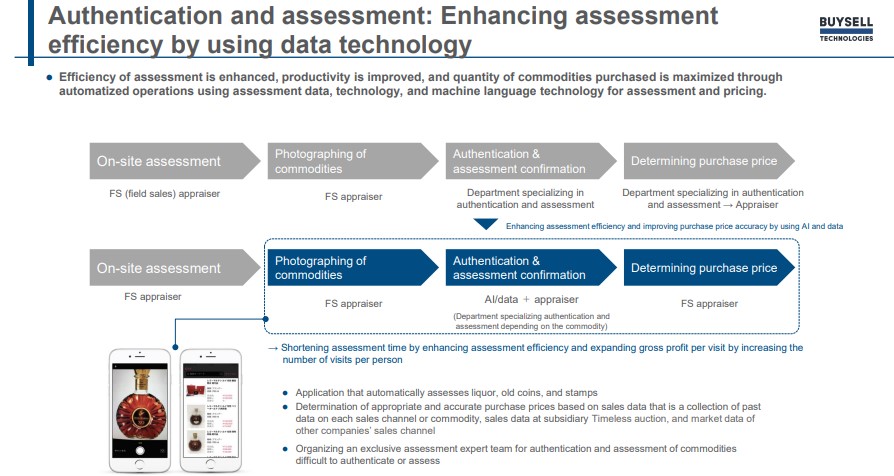

◎Authenticity Appraisal

To ensure accurate appraisal and prevention of counterfeit purchase and assessors' fraudulent appraisal, the Company's appraisal system requires not only an on-site appraisal by a visiting assessor but also a double check by another assessor who specialize in authenticity appraisal and appraisal, based on information from photos and videos sent from the visiting assessor using mobile terminals and such.

In addition, the company is using valuation data and technology to improve the efficiency and productivity of valuation and pricing decisions by automating operations using machine learning technology, etc., with the aim of maximizing the volume of purchases.

◎Products

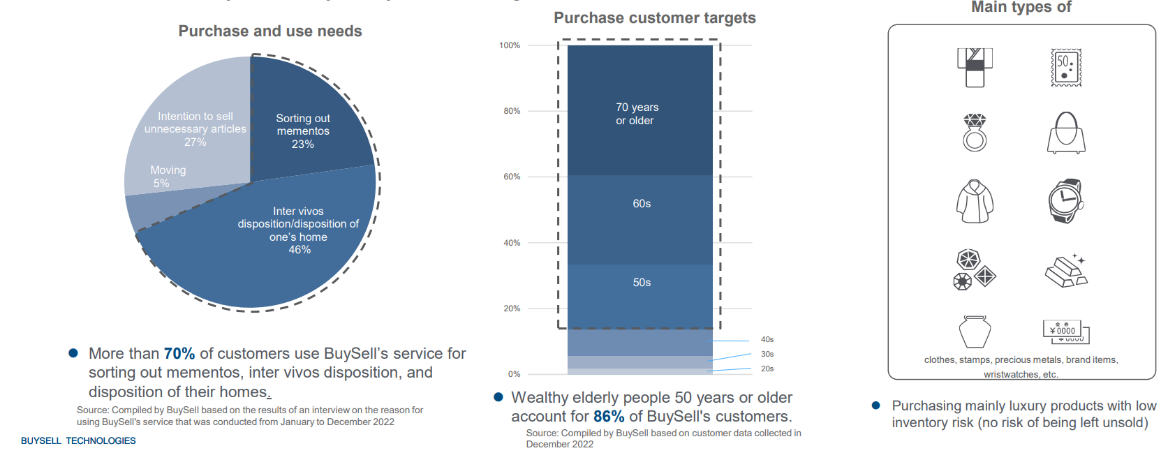

It deals with kimonos, stamps, old coins, precious metals, jewelry, brand-name items, watches, records, antiques, furs, alcoholic beverages and others, and focuses mainly on products with high selling prices.

(Source: the reference material of the Company)

◎Main Customers

There are many inquiries from senior wealthy people whose needs are aligned with the home visit purchase service, which is the Company's main service. In the FY ended December 2022, customers in their 50s and over accounted for approximately 86% of all customers.

In addition, senior customers use the Company's purchase services for disposition of one’s home, sorting out mementos and pre departure decluttering cleaning which account for approximately 70% of the reasons for using the services.

(Source: the reference material of the Company)

3) Sales:

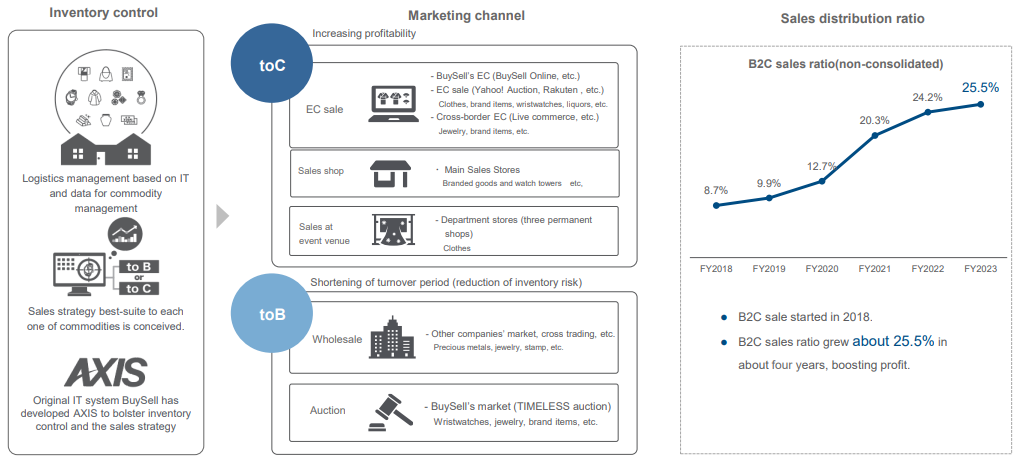

◎Inventory Management

After the cooling-off period, purchased products are managed centrally from inspection to exhibition by more than 300 staff including part-time job in the Company's own warehouse in Funabashi, Chiba Prefecture.

AXIS, an IT system developed by the Company, manages inventory for each product, and processes cooling-off requests.

The product is sent to the most suitable sales route, taking into account various aspects such as the characteristics and condition of the product as well as the market environment.

◎Sales System

After planning sales strategies based on inventory status, the Company sells purchased products through sales channels such as antique markets, auctions for dealers, e-commerce sales, special events and others.

For corporate sales through antique markets and auctions, the Company uses face-to-face auction formats for each product, and repeats negotiations with business partners until they find a sales partner that can produce a higher Profit Margin. In the fiscal year ended December 2023, approximately 74% of Sales comes from corporate customers.

In addition, the company holds an auction of kimonos regularly at Narashino Warehouse, and actualizes appropriate sales at each quality level and the distribution of more goods through TIMELESS Auction, which is held by TIMELESS Corporation, which was acquired as a subsidiary.

On the other hand, in sales to end-user general consumers, in order to provide high-quality products, the Company conducts EC sales (Rakuten Market, Yahoo! Auctions and others) and sales at department store events. It operates two e-commerce sites, "BuySell Online" which was launched in July 2018 and focuses on the sales of reused kimonos, and " BUYSELL brandchée ", which was opened on February 2020 and focuses on selling luxury reuse products such as brand-name items, watches, jewelry and alcoholic beverages. The company is also running a live commerce business for the Chinese market.

The Company aims to maximize Profits by expanding sales to general consumers while shortening the inventory turnover period (reducing inventory risk) through sales to corporations. The ratio of toC sales(non-consolidated), which started in 2018, was initially about 9%, but grew to 25.5% in fiscal year ended December 2023, driving profit growth.

By formulating optimal sales strategies for each product according to demand trend and building various sales channels, the Company is steadily accumulating results in sales, which is the third key to the success of the reuse business.

[1-5 Strengths and Features]

1) Maximization of synergy with a broad range of purchase and sales channels

The company is striving to maximize synergy by utilizing the strengths of the company and its subsidiary, TIMELESS, based on a wide array of purchase and sales channels of the two companies. Among many players in the reuse market, the Company has a unique business model which is unmatched by other competitors and constitutes a clear differentiator.

2) Strong Customer Base Centered on Senior Customers

As mentioned above, customers in their 50s and over make up approximately 86% of the Company's customer base. According to the Company's survey, 80% of the customers are satisfied with the responsiveness of the company's services, and the trust of senior high net worth individuals is strong.

This strong customer base will be a great advantage in future business development.

3) High Quality Management Team

One of the factors supporting the Company's growth is its excellent marketing strategy. According to Chairman Iwata, no other start-up can run TV commercials as cost-effectively as the Company.

Running successful TV commercials requires familiarity with the industry structure including which players exist and what kind of setups are required, but at the Company, Chairman Iwata who is from a major advertising company and have a great deal of knowledge, experience, and expertise, are strongly promoting a cross-marketing strategy.

In addition, in order to pursue sustainable growth by earning the trust of customers, it is essential to have a complete compliance system, and cash management in the purchase process is also an important point. Under the leadership of Director and CFO Mr. Koji Ono, the Company has been working to improve operations from an accounting perspective.

Mr. Masayuki Imamura, a director and CTO, has a proven track record of driving digital transformation across multiple companies, including well-known ones. He has led the expansion and growth of technology organizations to support data-driven management. Notably, his achievements were recognized with the "Findy Team+ Award" two years in a row, in 2022 and 2023, awarded to "companies with high productivity indicators for engineering organizations."

The Company runs its business with high quality management team, covering both offense and defense.

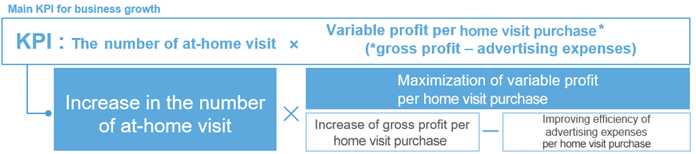

4) Main KPIs: "the number of at-home visit" x "Variable profit per home visit purchase "

The Company has set "the number of at-home visit" x "Variable profit per home visit purchase " as the main KPIs for the reuse business.

It pursues an increase in the number of inquiries by raising awareness in order to increase "the number of at-home visit", and seeks to maximize "Variable profit per home visit purchase " by increasing the purchase of high-priced products and optimizing advertising expenses.

(Source: the reference material of the Company)

2. The Second Quarter of Fiscal Year Ending December 2024 Earnings Results

(1) Business Results

| 2Q of FY 12/23 (cumulative total) | Ratio to Sales | 2Q of FY 12/24 (cumulative total) | Ratio to Sales | YoY | Company’s Forecast | Compared with the forecast |

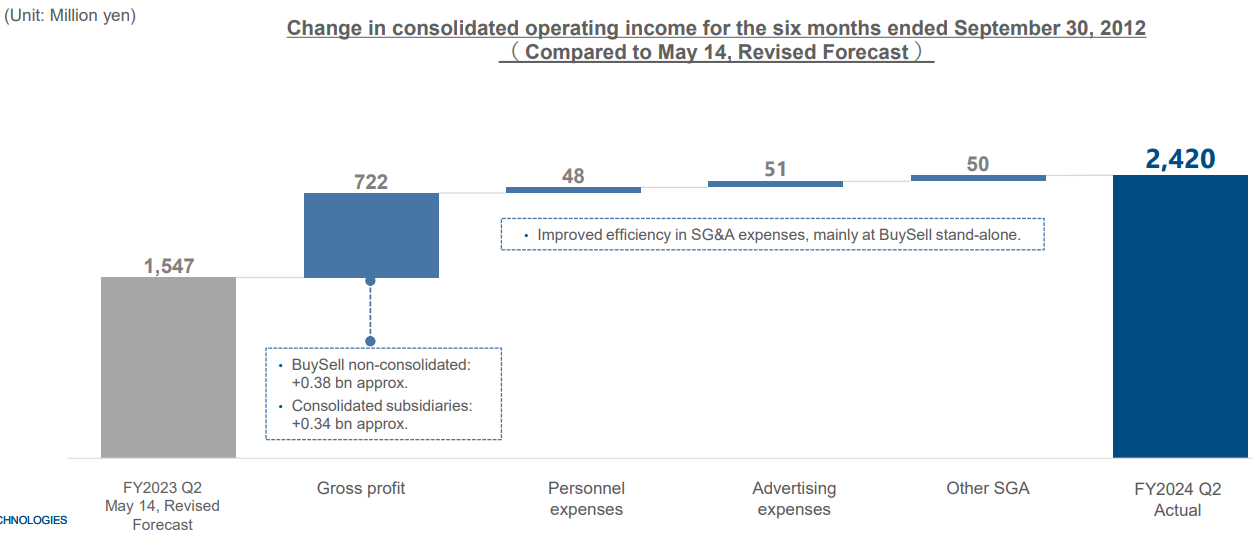

Net Sales | 19,561 | 100.0% | 28,720 | 100.0% | +46.8% | 27,263 | +5.3% |

Gross Profit | 11,449 | 58.5% | 15,329 | 53.4% | +33.9% | - | - |

SG&A | 10,136 | 51.8% | 12,909 | 45.0% | +27.4% | - | - |

Operating Income | 1,313 | 6.7% | 2,420 | 8.4% | +84.2% | 1,547 | +56.4% |

Adjusted EBITDA | 1,887 | 9.7% | 3,173 | 11.1% | +68.1% | 2,291 | +38.5% |

Ordinary Income | 1,291 | 6.6% | 2,307 | 8.0% | +78.6% | - | - |

Net Income | 635 | 3.3% | 1,210 | 4.2% | +90.4% | 767 | +57.7% |

* Unit: million yen.

Created by Investment Bridge based on disclosed material of the company.

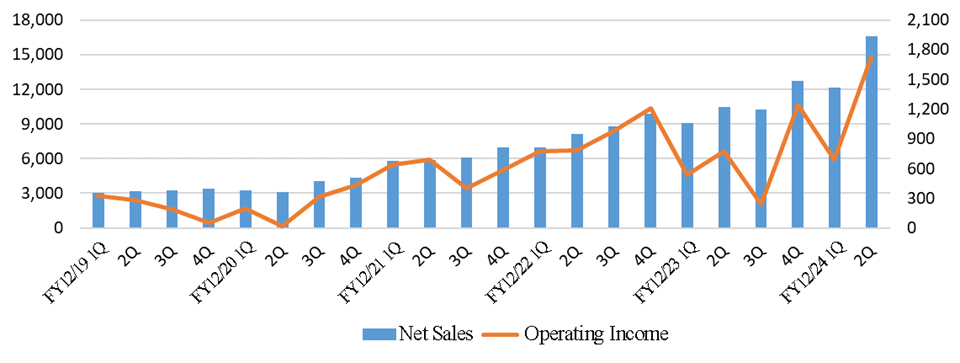

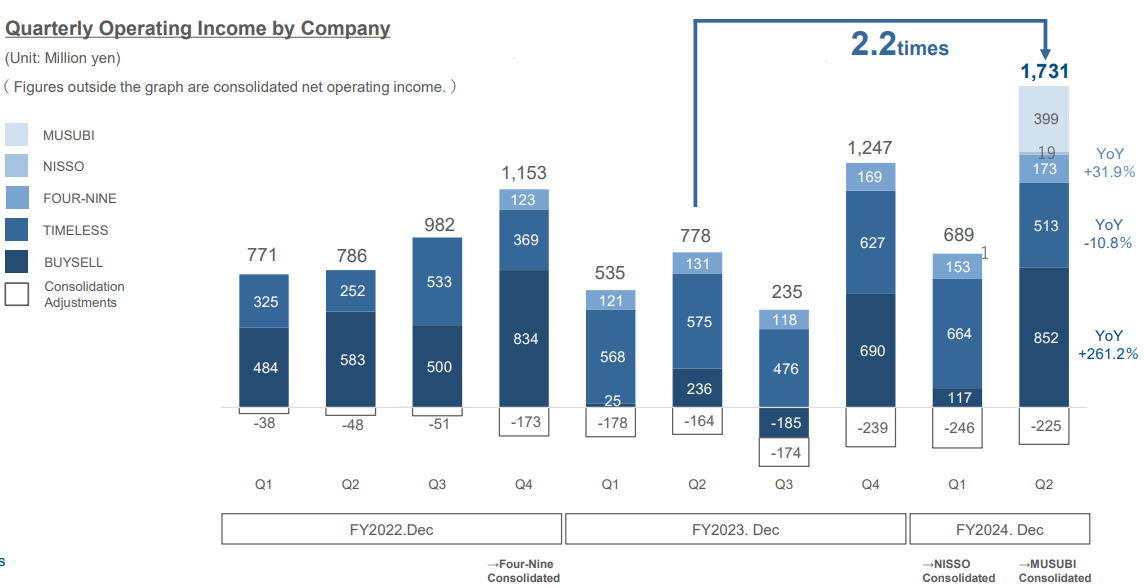

The cumulative results for 2Q of FY 12/2024 show a 46.8% year on year increase in sales, reaching 28,720 million yen, and an 84.2% year on year increase in operating income, amounting to 2,420 million yen. Compared to the revised budget disclosed in May (sales: 27,263 million yen, operating income: 1,547 million yen), the results exceeded expectations by 5.3% and 56.4%, respectively. Seeing these results in 2Q, the company once again revised its full-year forecast upwardly, after the earlier revision in May (sales: from 59,070 million yen to 61,850 million yen; operating income: from 3,800 million yen to 4,680 million yen). Additionally, Nisso Corporation joined the consolidated group in 1Q, and Musubi Corporation in 2Q. The impact of the inclusion of these new subsidiaries on the cumulative results in 2Q amounted to approximately 3.25 billion yen in sales and about 420 million yen in operating income (before goodwill amortization). With the effect of the inclusion of these subsidiaries, both sales and operating income in 2Q (three months) reached record highs.

Both the home visit purchase business and the in-store purchase business saw strong growth in purchase amount and sales. Considering the market environment, the company strategically increased its inventory, which contributed to the expansion in both sales and gross profit.

In terms of costs, although gross profit margin declined due to the impact of the inclusion of new subsidiaries and a change in the product mix due to the growth of precious metal purchase amount, the ratio of selling, general, and administrative expenses decreased, thanks to a reduction in the ratios of personnel and advertising expenses due to increased sales. As a result, operating income margin increased 1.7 points year on year, reaching 8.4%. Notably, Buysell's gross profit margin remained high at 64.8%.

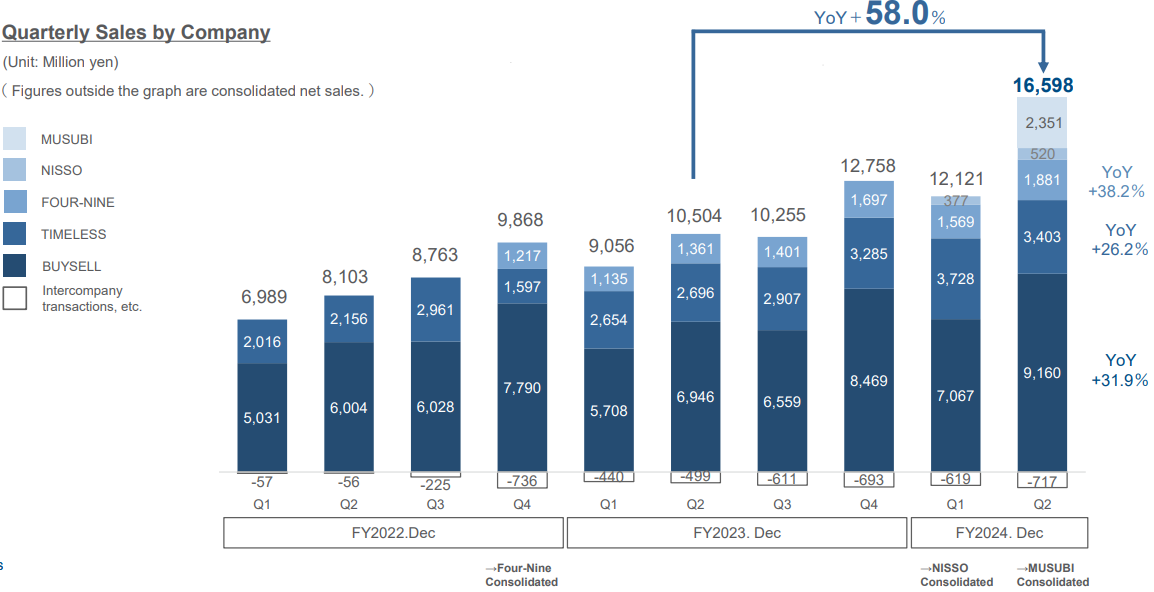

Sales in 2Q (three months) increased 58.0% year on year to 16,598 million yen. BuySell led the growth with a 31.9% increase, followed by Timeless with a 26.2% increase and Four Nine with a 38.2% increase. Additionally, the inclusion of Nisso and Musubi in the scope of consolidation contributed to this growth. Excluding the effect of these new subsidiaries, the actual year-on-year increase in revenue was 30.7%.

(Source: the reference material of the Company)

BuySell’s core business of home visit purchase, which had been strongly affected by the widespread robberies and the severe heat, has returned to normal, while the in-store purchase business has also been steadily expanding, leading to improved profitability. Although Timeless experienced a decline in operating income, this was due to strengthened investment in personnel and the postponement of some inventory sales to 3Q, which is in line with the plan. Not only has the impact of the new subsidiaries been realized, but synergies have also emerged after their involvement in the group’s business. As PMI progresses, further improvements in profitability are expected.

(Source: the reference material of the Company)

At the time of disclosure in 1Q, the company revised its forecast for the cumulative 2Q upwardly to reflect the results in 1Q and the impact of the inclusion of Musubi in the scope of consolidation. However, the results exceeded even those revised expectations. Specifically, strong sales of inventory purchased in 1Q in the home visit purchase business and better-than-expected performance by Musubi, due in part to transitory factors, boosted overall performance.

Analysis of operating income (Compared to Forecast)

(Source: the reference material of the Company)

(2) Trends in major KPIs for the home visit purchase service business

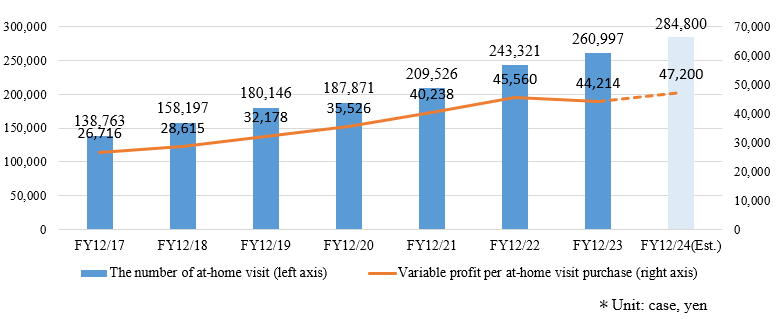

Created by Investment Bridge based on disclosed material of the company.

In addition to efforts from the start of the fiscal year to secure visit reservations for the upcoming months in preparation for the quieter summer season and the steady increase of repeat customers, there was no impact from a widespread robbery incident during this fiscal year, so the cumulative number of on-site visits in 2Q increased by 16.8% YoY. With strong results in both purchase and sales during 2Q, gross profit per on-site visit exceeded the company’s full-year forecast of 65,600 yen.

Advertising expenses per on-site visit continued to exceed the full-year forecast: 18,400 yen. While the competitive environment remains tough, some efficiency improvements have been realized, leading to an increase in variable profit per visit.

(3) Trends in major KPIs for the store business

Created by Investment Bridge based on disclosed material of the company.

By effectively leveraging group synergies through mutual customer introduction, marketing efforts, recruitment and HR strategies, and data integration, the company is promoting the operation of group stores while strengthening purchase channels that differentiate them from the on-site visit purchase business. As of the end of June 2024, the group had 356 stores.

(4) Financial Condition and Cash Flows

◎ Main BS (Consolidated)

| End of 12/23 | End of 6/24 | Increase and Decrease |

| End of 12/23 | End of 6/24 | Increase and Decrease |

Current Assets | 13,416 | 19,050 | +5,634 | Current Liabilities | 7,160 | 10,965 | +3,805 |

Cash Equivalent | 7,756 | 11,003 | +3,247 | ST Interest Bearing Liabilities | 2,909 | 5,909 | +3,000 |

Inventories | 4,543 | 6,651 | +2,108 | Non-current Liabilities | 5,550 | 10,944 | +5,394 |

Noncurrent Assets | 7,904 | 12,448 | +4,544 | LT Interest Bearing Liabilities | 5,159 | 10,591 | +5,432 |

Tangible Assets | 1,148 | 1,493 | +345 | Liabilities | 12,710 | 21,909 | +9,199 |

Intangible Assets | 5,695 | 9,609 | +3,914 | Net Assets | 8,610 | 9,589 | +979 |

Investment, Others | 1,059 | 1,346 | +287 | Retained Earnings | 6,038 | 6,891 | +853 |

Assets | 21,320 | 31,499 | +10,179 | Total Liabilities and Net Assets | 21,320 | 31,499 | +10,179 |

* Unit: million yen

Created by Investment Bridge based on disclosed material of the company.

Inventory increased 2,108 million yen from the end of the previous period to 6,651 million yen. Both BuySell and Timeless saw strong purchase performance, which contributed to an increase in inventory by 1.4 billion yen from the end of the previous fiscal year. Additionally, the inclusion of new subsidiaries significantly contributed to the increase. However, since sales were strong, the inventory turnover period remained unchanged from the end of the previous fiscal year.

The main factor behind the increase in fixed assets was the posting of goodwill of Musubi (¥4.1 billion, amortized over 17 years). Interest-bearing debt increased due to borrowing to finance the M&A of Musubi and for working capital, resulting in a decline in equity ratio from 39.5% at the end of the previous fiscal year to 29.6%.

◎Cash Flow(Consolidated)

| 2Q of FY 12/23 | 2Q of FY 12/24 | Increase and Decrease |

Operating cash flow(A) | 917 | 812 | -105 |

Investing cash flow(B) | -707 | -5,290 | -4,583 |

Free cash flow(A+B) | 209 | -4,478 | -4,688 |

Financing cash flow | 1,029 | 7,730 | +6,701 |

Cash and Equivalents at the end of term | 8,244 | 10,934 | +2,690 |

* Unit: million yen

Created by Investment Bridge based on disclosed material of the company.

In addition to interim net income before taxes and other adjustments of 2,307 million yen, an increase of 645 million yen in depreciation, amortization of goodwill, and depreciation of customer-related assets was offset by an increase of 271 million yen in trade receivables, 1,563 million yen in inventories, and 639 million yen in income taxes paid, resulting in operating cash flow of 812 million yen.

Investment cash flow saw an outflow of 5,290 million yen. In addition to 4,669 million yen spent for the acquisition of shares in subsidiaries resulting in a change in the scope of consolidation, 193 million yen was spent for the acquisition of tangible fixed assets related to the opening of new stores, etc., and 374 million yen was spent for the acquisition of intangible fixed assets related to the development of in-house systems.

Financial cash flow saw an inflow of 7,730 million yen, which included 1,500 million yen from short-term borrowings and 8,300 million yen from long-term borrowings. As a result, the cash and cash equivalents at the end of the interim consolidated accounting period was 10,934 million yen.

(5) Topics

Acquisition of REXT HOLDINGS Co., Ltd. as a subsidiary

The company plans to acquire 100% of the shares of REXT HOLDINGS Co., Ltd. through a two-step process involving cash payment and share exchange. Specifically, it will first acquire 88.5% of the shares by paying 8.2 billion yen in cash (with the acquisition date set for October 1, 2024), and then acquire the remaining 11.5% through a share exchange (with an acquisition price of 1.07 billion yen and the share exchange scheduled for completion on October 8, 2024). A total of 297,000 shares will be allocated in the share exchange, with an exchange ratio of 1:297, all of which will be allocated from treasury shares. The cash will be procured through borrowing. The company plans to include Rext Holdings into its balance sheet from 4Q of FY 12/2024 and into its profit and loss statement from 1Q of FY 12/2025. The amount of goodwill and the number of years for amortization of goodwill have not yet been determined at this stage.

REXT HOLDINGS Co., Ltd. owns reuse-related companies and functional companies such as REGATE Corporation, which operates the home visit purchase service "Buy Fuku-chan" and Nikkodo Corporation, which operates an antique purchase business. The company's consolidated financial results (LTM estimate) for FY 12/2024 are as follows:

The company has 13,770 million yen in sales, 1,155 million yen in EBITDA, and 971 million yen in operating income, indicating a reasonable scale. The core company, REGATE Corporation, has 93,000 business trip visits (FY12/2023), which is more than 1/3 of the size of BuySell alone. As of the end of June 2024, the group had 18 stores. The company believes that by integrating the home visit purchase business group and the Rext Holdings group into a single group, they can generate synergies such as improving efficiency in advertising expenses, enhancing logistics through mutual collaboration, optimizing sales channels for greater profitability, strengthening the handling of antiques, improving strategy and human resources through data-driven management, and achieving more efficient operations and profitability through digital transformation (DX) initiatives.

3. Fiscal Year Ending December 2024 Earnings Forecasts

(1) Business Results

◎Consolidated Financial Forecast

| FY 12/23 | Ratio to Sales | FY 12/24 (Initial Est.) | Ratio to Sales | FY 12/24 (Revised Est.) | Ratio to Sales | YoY |

Net Sales | 42,574 | 100.0% | 52,480 | 100.0% | 61,850 | 100.0% | +45.3% |

Gross Profit | 24,493 | 57.5% | 29,125 | 55.5% | 32,651 | 52.8% | +33.3% |

SG&A | 21,696 | 51.0% | 25,725 | 49.0% | 27,971 | 45.2% | +28.9% |

Operating Income | 2,796 | 6.6% | 3,400 | 6.5% | 4,680 | 7.6% | +67.4% |

Adjusted EBITDA | 3,994 | 9.4% | 4,910 | 9.4% | 6,332 | 10.2% | +58.5% |

Ordinary Income | 2,754 | 6.5% | 3,310 | 6.3% | 4,140 | 6.7% | +50.3% |

Net Income | 1,453 | 3.4% | 1,890 | 3.6% | 2,240 | 3.6% | +54.1% |

*Unit: million yen.

No change in positioning as a period for laying the foundation for the next medium-term management plan

At the beginning of the fiscal year, the budget was formulated at a realistic level, taking into account the previous year’s performance and the business environment outlook. However, in reality, the negative factors affecting the home visit purchase business have diminished, and the business environment was showing signs of improvement. As a result, following the upward revision in May, the full-year company plan was once again revised upwardly in August, reflecting the recent performance. Specifically, the upwardly revised forecast calls for sales increasing 45.3% YoY to ¥61,850 million, operating income rising 67.4% YoY to ¥4,680 million, and adjusted EBITDA increasing 58.5% YoY to ¥6,332 million. The dividend forecast per share has been raised from 25 yen/share to 30 yen/share. The company maintains its stance, viewing FY 12/2024 as a period of preparation for a high growth phase from FY 12/2025 onward, with the strategic goal of increasing operating income per employee.

In the home visit purchase business, the focus is on improving the efficiency of marketing investments, which had worsened in terms of cost-effectiveness during the previous fiscal year. While reducing sales-to-advertising ratio from 15.3% in the previous fiscal year to 12.7%, the company plans to increase the number of on-site visits by 9% YoY to 284,800.

Regarding the in-store purchase business, the company plans to actively expand its business, including through M&A strategies. Beyond simply increasing the number of stores through M&A, the plan also involves enhancing collaboration between group stores to improve efficiency in opening new stores and strengthen sales channels.

The company also plans to make upfront investments for FY 12/2025 and beyond. Specifically, the company plans to invest in the opening of flagship stores to strengthen direct-to-consumer sales, the expansion of overseas sales channels, and the strengthening of its own e-commerce.

Regarding the current medium-term management plan, the plan for the fiscal year ending December 2024 will be replaced with the company's forecast announced this time, and no qualitative changes will be made. The company will continue to work on the final year based on the medium-term management plan announced earlier and plans to announce a new medium-term management plan at the time of the announcement of the full-year financial results for the fiscal year ending December 2024, scheduled in February 2025.

4. Conclusions

As the worst period of the external environment has obviously ended, the company appears to be adopting a more assertive stance. While recent performance has been healthy, the management is focusing on the future. The capital market should look beyond short-term results to the company's growth potential. These upfront investments indicate the company’s intention to take a step beyond the purchase domain. The secondary distribution market in Japan is significant. Moreover, considering the high value placed on Japanese secondary distribution goods, particularly in Asia, there is an expectation that these investments will further expand the company’s total addressable market (TAM).

<Reference: Regarding Corporate Governance>

◎Organization type, and the composition of directors and auditors

Organizational Type | Company with Audit & Supervisory Committee |

Directors | 12 directors, including 6 outside directors |

Audit & Supervisory Committee | 3 members, including 3 outside members |

◎Corporate Governance Report

The latest revision date: April 1, 2024

<Fundamental Concept>

The Company recognize that establishing corporate governance is essential in order to increase corporate value, maximize shareholder returns, and build good relationships with stakeholders such as customers, business partners, employees, local communities, and government agencies.

To this end, the Company believe that it is important to establish a decision-making body that responds quickly and fairly to changes in the business environment, pursue Profits through its businesses, ensure that its financial soundness and improve its credibility, actively disclose information to fulfill accountability, build an effective internal control system, and ensure that audit and supervisory committee members maintain their independence and fulfill their audit functions.

<Reasons for not implementing each principle of the Corporate Governance Code>

The Company has implemented all the basic principles of the Corporate Governance Code.

This report is not intended for soliciting or promoting investment activities or offering any advice on investment or the like, but for providing information only. The information included in this report was taken from sources considered reliable by our company. Our company will not guarantee the accuracy, integrity, or appropriateness of information or opinions in this report. Our company will not assume any responsibility for expenses, damages or the like arising out of the use of this report or information obtained from this report. All kinds of rights related to this report belong to Investment Bridge Co., Ltd. The contents, etc. of this report may be revised without notice. Please make an investment decision on your own judgment. Copyright(C) Investment Bridge Co., Ltd. All Rights Reserved. |